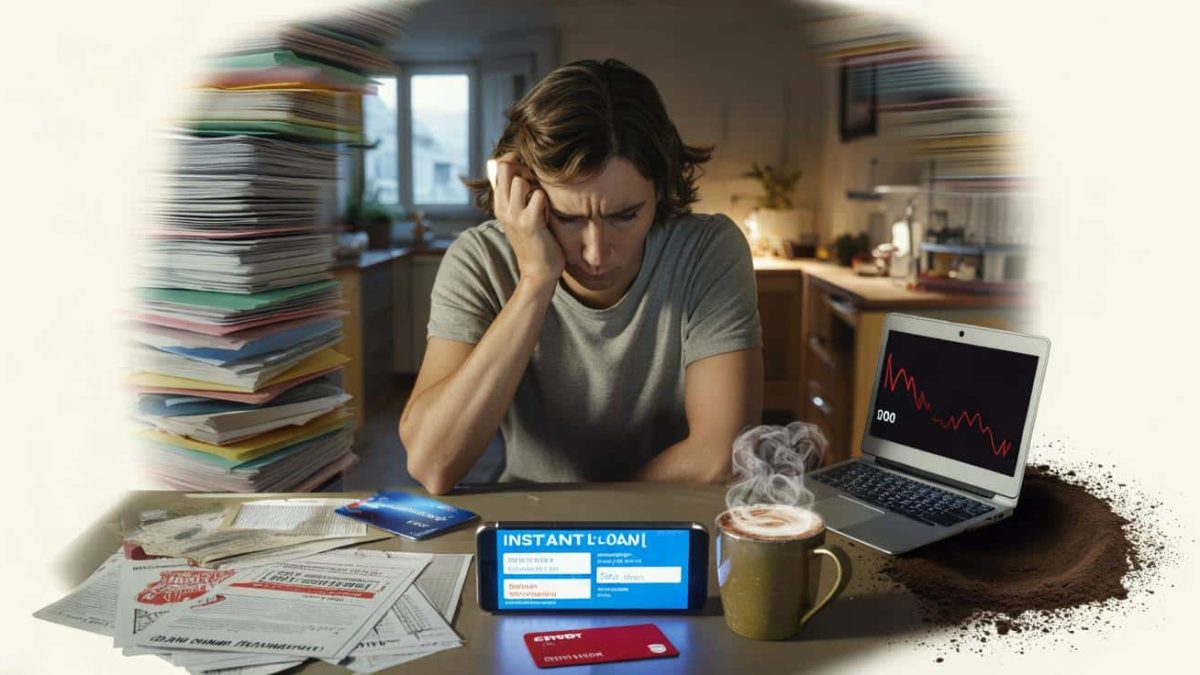

As you sit there, sipping your now-cold coffee, your banking app glares back at you. Three outstanding bills, a negative balance, and a maxed-out credit card. It’s a familiar story for many – the vicious cycle of debt that just never seems to end. But what if we told you that taking out a loan to pay off other debts could actually make the situation worse? That’s the harsh reality that too many people are facing, and it’s time to break the cycle before it breaks you.

The Dangerous Debt Spiral: How Loans Can Trap You

It’s a tempting solution, isn’t it? When you’re drowning in bills and overdue payments, the idea of consolidating everything into a single loan with a lower interest rate can seem like a lifeline. But the reality is that this approach often backfires, leading to an even deeper financial hole. The problem is that without a well-thought-out plan, you’re simply moving the problem around instead of addressing the root cause.

The truth is, taking out a loan to pay off other debts is a bit like rearranging deck chairs on the Titanic. It might feel like you’re making progress, but the underlying problem – the unsustainable spending habits or lack of budgeting – is still there, just hidden behind a new loan. And as the interest accrues and the payment due dates roll around, the situation can quickly spiral out of control.

Before you know it, you’re right back where you started, or even worse off, with a new loan to worry about on top of the old debts. It’s a vicious cycle that can be incredibly difficult to break free from, and the longer it goes on, the harder it becomes to see a way out.

- ➡The Shocking Truth About Exercise and Osteoarthritis Treatment You Need to Know

- ➡The Shocking Secret Treasure Discovered at the Bottom of the Sea (and Why the Finder Went to Prison)

- ➡Shocking Secrets to Restore Peace in a Multi-Cat Home That Nobody Told You

- ➡The Scandalous Balcony Bloom That’s Dividing Germany’s Green Thumbs

- ➡Unearthed Ancient Highway Stuns Experts—Uncover the Secrets of This 2,200-Year-Old Marvel

- ➡The Astonishing Homemade Trick That’s Reshaping Skin After 60 (You Won’t Believe This!)

- ➡The Unbelievable Flower That Turned My Doorstep Into a Local Sensation

- ➡The Subscription Trap: The Hidden Charges Draining Your Bank Account

The Hidden Costs of Debt Consolidation Loans

One of the biggest misconceptions about debt consolidation loans is that they automatically save you money. While it’s true that the interest rate may be lower than what you were paying on your credit cards, there are often hidden costs and fees that can quickly erode any potential savings.

For starters, the loan itself will likely come with an origination fee, which can be anywhere from 1% to 6% of the total loan amount. That means if you’re borrowing $20,000, you could be paying upwards of $1,200 just to get the loan in the first place. And then there’s the matter of the repayment period – these loans often have much longer terms than credit cards, which means you’ll be paying interest for a longer period of time.

But perhaps the most dangerous aspect of debt consolidation loans is the false sense of security they can provide. It’s easy to get lulled into a false sense of progress, thinking that the problem has been solved, when in reality, you’re just postponing the inevitable. And if you’re not careful, you could end up right back where you started, or even worse off, with a new loan to worry about on top of the old debts.

The Importance of a Solid Plan

If you’re considering a debt consolidation loan, it’s crucial that you have a solid plan in place before you sign on the dotted line. This means taking a long, hard look at your spending habits, creating a detailed budget, and identifying the root causes of your debt in the first place. Without a clear plan for how you’re going to pay off the loan and break the cycle of debt, you’re just setting yourself up for failure.

- ➡NASA Uncovers Shocking Martian Secrets: The Real Reason We May Not Be Alone

- ➡Shocking Footage Exposes Neighbor’s Sinister Scheme to Spy on Single Mom’s “Secret Life”

- ➡4 Short Hairstyles That’ll Transform Your Thin Hair Into Thicker-Looking Locks

- ➡The Shocking 2,000-Year-Old Decision That Transformed Our Legal Rights Forever

- ➡Shocking Trick to Transform Your Mornings and Conquer the Day

- ➡The Shocking Collapse of Greenland’s Ice and the Surprising Rise of Orcas

- ➡The Silent Scrollers: What Your Lurking Habit Really Says About You

- ➡The Surprising Cause of Social Anxiety (And How to Overcome It)

One of the key things to consider is whether the loan will actually save you money in the long run. If the interest rate is still higher than what you were paying on your credit cards, or if the repayment period is longer, then it may not be worth it. You’ll also need to factor in the impact of the loan on your credit score, as taking on a new debt can temporarily lower your score and make it harder to qualify for other loans or credit in the future.

Ultimately, the decision to take out a debt consolidation loan should be carefully considered and based on a thorough understanding of your financial situation and a clear plan for how you’re going to pay it off. Without that foundation, you’re just setting yourself up for more financial stress and uncertainty down the road.

Breaking the Cycle: Alternative Strategies for Debt Relief

If a debt consolidation loan isn’t the right solution for you, there are other strategies you can explore to help break the cycle of debt. One option is to work with a credit counseling service, which can help you negotiate with your creditors and create a debt management plan. This can often result in lower interest rates and more manageable monthly payments, without the need for a new loan.

Another approach is to try a balance transfer credit card, which allows you to transfer your high-interest debt to a new card with a 0% introductory APR. This can give you some breathing room to pay down the balance without accruing additional interest, but it’s important to have a plan in place to pay off the debt before the promotional period ends.

- ➡Shocking Discovery Under Antarctica’s Ice Could Reshape the World!

- ➡You’ll Never Believe These 5 Bob Haircuts That Can Age You After 40

- ➡Shocking Astrology Forecast for March 22, 2026: These Zodiac Signs Will Experience a Major Turning Point

- ➡The Simple Financial Snapshot That Prevents Nasty Surprises in the New Year

- ➡Endangered Cub’s First Steps Spark Celebration at Zoo—You Won’t Believe What Happened Next!

- ➡The Shocking Tax Loophole Retirees Are Using to Escape Taxes (You Won’t Believe What Happened Next!)

- ➡Unlock the Secret to a Thriving Oasis: How to Build a Mesmerizing Mini-Pond on Your Balcony

- ➡China’s Secret Invisibility Material Just Changed Everything—Here’s What We Know

And of course, there’s the good old-fashioned approach of cutting back on expenses, increasing your income, and dedicating as much as possible to paying down your debts. It may not be the easiest path, but it’s often the most sustainable in the long run.

The Real Cost of Debt: Beyond the Numbers

The financial toll of debt is well-documented, but the emotional and psychological impact can be just as devastating. Stress, anxiety, and feelings of hopelessness are all too common for those trapped in the debt cycle. And the longer it goes on, the harder it can be to see a way out.

But it’s important to remember that you’re not alone. Millions of people around the world are struggling with similar challenges, and there are resources and support available to help you get back on track. Whether it’s a credit counseling service, a support group, or a financial coach, don’t be afraid to reach out and seek help.

Because at the end of the day, the true cost of debt goes far beyond the numbers on your balance sheet. It’s about your mental and emotional well-being, your relationships, and your ability to live the life you truly want. And that’s a price that no one should have to pay.

- ➡The Unbelievable Journey of a $20 Painting That Sold for $4.2 Million

- ➡Shock Revealed: The Surprising Psychology Behind Wearing a Crossbody Bag

- ➡The Surprising Truth About Sweet Potatoes and Regular Potatoes: A Shocking Divide Splitting Experts Right Down the Middle

- ➡Unearthing the Hidden Wonders Beneath the Swiss Alps: A Secret Network of Tunnels Redefining Infrastructure

- ➡You’ll Never Guess How Long This Once-in-a-Lifetime Solar Eclipse Will Last!

- ➡Is Frying with Olive Oil Really Healthy? The Experts Answer

- ➡The Shocking Laundry Hack That’s Splitting Households and Saving Tons of Energy

- ➡Shocking Secrets Emerge as the Netherlands Reshapes Its Coastline: A Decade-Long Battle Between Progress and Preservation

The Path Forward: Building a Sustainable Financial Future

The journey out of debt may not be an easy one, but it is absolutely possible. By taking a proactive approach, developing a solid plan, and staying disciplined, you can break the cycle and build a sustainable financial future for yourself and your loved ones.

It all starts with understanding your financial situation, setting clear goals, and creating a realistic budget that you can stick to. From there, it’s about finding creative ways to increase your income, reduce your expenses, and pay down your debts as quickly as possible. And don’t be afraid to seek out help and support along the way – there are many resources and experts who can guide you through the process.

Remember, the path to financial freedom is not a sprint, but a marathon. It may take time and effort, but the rewards are well worth it. By breaking the debt cycle and taking control of your financial future, you’ll not only find greater peace of mind, but you’ll also be able to invest in the things that truly matter – your passions, your relationships, and your dreams.

Frequently Asked Questions

Is a debt consolidation loan always a bad idea?

Not necessarily, but it’s important to approach it with caution and a clear plan. A debt consolidation loan can be helpful if it results in a lower interest rate and more manageable monthly payments, but it’s crucial to have a solid strategy for paying off the loan and avoiding falling back into the debt cycle.

- ➡Shocking Truth: The Zero-Oil Secret That’s Obliterating Air Fryers

- ➡The Secret Hack to Revive Curtains Without Washing Them

- ➡The Shocking Secrets Hiding in China’s Desert Oasis: How Trees Are Saving the Planet

- ➡Shocking NASA Rover Data Reveals the Unexpected Truth About Life on Mars

- ➡Revealed: The Secret Rhetorical Trick to Shut Down Attackers in One Sentence

- ➡The Shocking Truth About Winter Hair Loss (and How to Stop It)

- ➡The Unbreakable Asian Fruit Tree Taking the Gardening World by Storm

- ➡Poultry Pandemonium: 3,000 Hens Rescued from Slaughter, Urgent Need for New Homes!

How can I create a realistic budget to pay off my debts?

Start by tracking your income and expenses, and identify areas where you can cut back. Prioritize your debts and create a payment plan that dedicates as much as possible towards the highest-interest debts. Consider using budgeting apps or working with a financial advisor to help you stay on track.

What are some alternative strategies to debt consolidation loans?

Some alternatives include working with a credit counseling service, transferring balances to a 0% APR credit card, and focusing on increasing your income and reducing expenses to pay down debts faster. It’s also important to address the root causes of your debt, such as overspending or lack of budgeting.

How can I improve my credit score after paying off debts?

Paying off debts and maintaining a clean credit history is the best way to improve your credit score over time. Be sure to keep credit card balances low, make payments on time, and avoid taking out new loans or credit unless absolutely necessary.

What are the long-term consequences of debt?

Unmanaged debt can have a significant impact on your financial and personal well-being, including higher stress levels, strained relationships, and limited opportunities for saving and investing. It’s crucial to prioritize paying off debts and developing healthy financial habits to avoid these negative consequences.

- ➡The Shocking Anti-Aging Secret Seniors Are Hiding From You

- ➡Shocking Discovery on Mars: NASA Rover Uncovers Ancient River Traces Beneath the Surface

- ➡Shocking Twist! Australia’s Submarine Deal Implodes, Leaving Them High and Dry

- ➡The Shocking Eco-Friendly Habits Sabotaging the Planet

- ➡The Shocking Truth About How Tipping Is Ruining America

- ➡The Secret Superpower Keeping France a Maritime Mapping Juggernaut for Over 305 Years

- ➡Butter Shock: The Staple That’s Now a Luxury for Many Shoppers

- ➡The Shocking Trick That Could Save You €60 on Your Electricity Bill This Winter

How can I stay motivated to pay off my debts?

Set realistic goals, celebrate small wins, and remind yourself of the long-term benefits of being debt-free. Seek support from friends, family, or a financial advisor to help you stay accountable and on track. Remember, the journey may be challenging, but the rewards of financial freedom are well worth it.

What should I do if I’m struggling to make debt payments?

Reach out to your creditors as soon as possible to discuss your options, such as negotiating a payment plan or temporary relief. Consider working with a credit counseling service or a financial advisor to help you navigate the situation and explore alternative solutions.

How can I prevent falling into the debt trap again in the future?

Develop healthy financial habits, such as budgeting, saving, and limiting unnecessary spending. Avoid taking on new debts unless absolutely necessary, and be mindful of the long-term consequences of any financial decisions. Regularly review your financial situation and make adjustments as needed to maintain financial stability.