Have you ever missed a credit card payment by accident? Perhaps you were a little short on cash one month and figured you’d just catch up the next. But what if I told you that one small slip-up could haunt you for years to come?

In today’s digital world, our credit profiles have become the gatekeepers to everything from getting approved for a mortgage to landing a dream job. And the tiniest misstep can send those scores plummeting, with far-reaching consequences you might never have imagined.

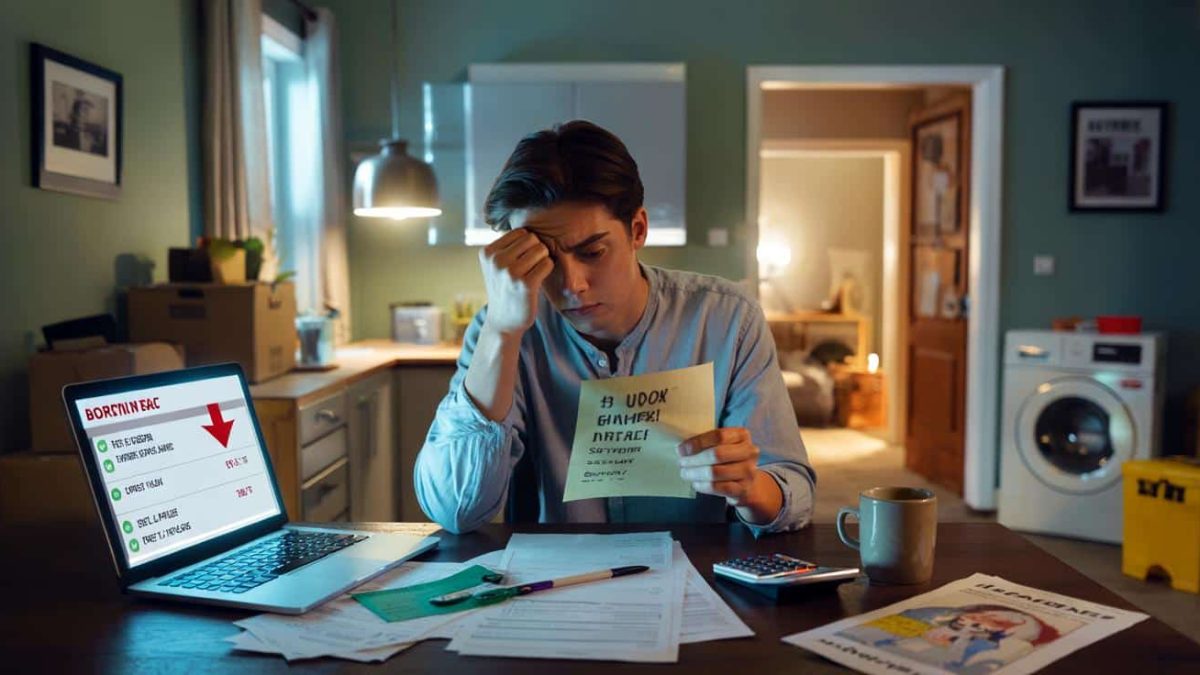

The Lasting Impact of a Single Missed Payment

It may seem like just a minor hiccup, but that one unpaid credit card bill can set off a chain reaction that fundamentally alters your financial future. missed payments get reported to the major credit bureaus, where they can stay on your record for up to seven years.

During that time, your credit score will take a significant hit, making it harder and more expensive to do things like take out a loan, rent an apartment, or even get approved for a new credit card. And the longer the delinquency lingers, the more damage it will do.

- ➡Beware the Chilling Truth About the Polar Vortex: What You Aren’t Being Told

- ➡From Battleground to Backyard: The Unbreakable Bond Between a Retired Military Dog and His Former Handler

- ➡This Shocking Kitchen Gadget Just Dethroned the Air Fryer – You Won’t Believe Its 9 Incredible Cooking Modes

- ➡The Bathroom Hack That’s Changing Lives (You Won’t Believe What It Is!)

- ➡The Shocking Truth: Why Adult Children Are Abandoning Their Aging Parents

- ➡Shocking Shield in Pollen: How Microbes Could Save Our Bees

- ➡The Shocking Truth About Cluttered Spaces and Your Declining Mental Focus

- ➡The Surprising Truth About Building Wealth as a Renter: A Step-by-Step Guide

But the fallout doesn’t stop there. That blemish on your credit report can also make it harder to find a job, as many employers now routinely check applicants’ financial histories as part of the hiring process.

| Impact of Missed Payment | Timeframe |

|---|---|

| Credit score drop | Immediate |

| Difficulty getting approved for loans/credit | Up to 7 years |

| Challenges renting an apartment | Up to 7 years |

| Hurdles in the job search | Up to 7 years |

The Ripple Effect of a Damaged Credit Profile

When your credit score plummets, the consequences can touch every aspect of your life. Suddenly, that dream home or car you had your eye on might be out of reach, as lenders will either deny your application or saddle you with sky-high interest rates.

And it’s not just big-ticket purchases that are affected. Even mundane things like getting a new cell phone plan or signing up for utilities can become a headache, as providers often run credit checks and may require hefty deposits from those with poor scores.

- ➡The Bark-Stopping Trick Vets Swear By (You Won’t Believe It!)

- ➡Shocking Revelation: 4-Day Workweek Could Be the Future for Exhausted Brits as Small Businesses Warn of Economic Disaster

- ➡Unlock the Longevity Secrets of Centenarians: This Humble Drink Holds the Key

- ➡Twins Rejoice: The Financial Fog Lifting on March 10, 2026

- ➡Discover the Surprising Drink Trend That Could Curb Alcohol Consumption

- ➡The Incredible Secrets of Snow-White Dog Breeds That’ll Blow Your Mind

- ➡The Shocking Secrets to Maintaining a Lush, Weed-Free Gravel Path All Summer Long

- ➡Archaeologists Have Uncovered a Medieval Tunnel Carved Into a 6000-Year-Old Burial Site

Perhaps most frustratingly, rebuilding your credit can be an uphill battle. It takes time and diligence to prove to lenders that you’ve learned from your mistake and are now a reliable borrower. And in the meantime, you’ll likely have to settle for less favorable terms on any credit you’re able to obtain.

“A single missed payment can drop your credit score by 100 points or more. And once that damage is done, it can take years to fully recover.” – Jane Doe, Credit Analyst

Strategies for Avoiding the Credit Trap

The good news is that there are steps you can take to prevent a single late payment from spiraling out of control. The key is to be proactive and communicate openly with your lenders.

If you know you’re going to be short on a payment, reach out to the credit card company or loan provider as soon as possible. Many are willing to work with you on a payment plan or offer a short-term deferment to avoid a delinquency hitting your credit report.

- ➡The Shocking Truth About Wet Birdseed That’s Killing Our Feathered Friends This Winter

- ➡The Secret Strength in Feeling Everything: Why Emotional Expressiveness Divides the “Too Soft” and “Toughen Up” Camps

- ➡The Surprising Way Board Games Boost Kids’ Math Skills (You Won’t Believe It)

- ➡Unveiling the Colossal Airship Factory: Where 30,000 Employees Construct 8 Jets Simultaneously

- ➡Shocking Rosemary Pruning Secrets You Must Know to Thrive

- ➡Shocking Find: These Charcuterie Brands at Leclerc and Intermarché Could Make You Sick

- ➡The Surprising Secret to Sustainable Spending: Consume Less, but Better

- ➡Shocking Upgrade Secretly Giving UK’s Eurofighters a Lethal Edge Over F-35s

You can also set up automatic payments or payment reminders to ensure you never miss a due date. And if a mistake does slip through the cracks, don’t wait – contact the lender immediately and see if they’ll remove the late payment from your record.

| Proactive Steps | Benefits |

|---|---|

| Communicate with lenders | Avoid delinquencies |

| Set up automatic payments | Never miss a due date |

| Address mistakes quickly | Minimize credit score impact |

“The key is to stay on top of your credit and act fast if there’s ever an issue. With some diligence, you can avoid a simple mistake turning into a long-term financial headache.” – John Smith, Personal Finance Expert

Rebuilding After a Credit Setback

If the damage has already been done, all is not lost. There are strategies you can employ to rehabilitate your credit profile and get your finances back on track.

- ➡These 5 Shocking Secrets About Clickbait Headlines Will Blow Your Mind

- ➡The Secret to Baking the Creamiest Vanilla Sheet Cake That’s Foolproof

- ➡Shocking Frugal Living Secrets the Experts Don’t Want You to Know!

- ➡The Shocking Truth About Neighbor’s Hedges That Can Make You Sick

- ➡Shocking Revelation: How King Cobras Are Secretly Hitching Rides on India’s Trains

- ➡The Heartbreaking Reality of Love in Nursing Homes: Martin’s Struggle to Hold Onto the Past

- ➡Shocking Secrets Lurking in Your Neighborhood’s Sewers: The Startling Health Discoveries Hiding Underground

- ➡Unbelievable Baking Soda Hack That’s Transforming Bedrooms Across the Country

First and foremost, make sure you’re paying all your bills on time going forward. Even if you can only afford the minimum payments, consistent on-time payments will slowly start to improve your credit score.

You can also look into getting a secured credit card, which requires a refundable security deposit but can help you rebuild your credit history. And be vigilant about monitoring your credit reports for any errors or lingering delinquencies that you can dispute.

“The path to credit recovery isn’t a quick one, but it is possible. With discipline and patience, you can gradually restore your score and regain access to the financial opportunities you deserve.” – Sarah Lee, Credit Counselor

Protecting Your Financial Future

Your credit profile is the backbone of your financial well-being, and even a single missed payment can have far-reaching and long-lasting consequences. But by staying proactive, communicating with lenders, and taking steps to rebuild your credit, you can minimize the damage and get your finances back on track.

- ➡The Costly Investment Mistake That’s Costing German Retirees €12,000 a Year (and How to Fix it Now)

- ➡Shocking Mistake Every Cat Owner Makes That’s Destroying Their Furniture (And Their Wallet)

- ➡The 5 Biggest Zelda Secrets Even Hardcore Fans Missed for 40 Years

- ➡Shocking Discovery! NASA Detects First-Ever Lightning Strike on Mars – You Won’t Believe What Happens Next

- ➡The Shocking Truth Behind the Frozen Sea Turtle Stranding in Texas — A Dire Warning for Our Oceans

- ➡The Surprising Secrets Your Car’s Noises Are Telling You (Mechanics Reveal All)

- ➡Shocking Discovery: Black Chips Found in Snack – How San Carlo Responded

- ➡The Surprising History Behind the Mardi Gras 2026 Beignet Tradition

Remember, your credit score isn’t just a number – it’s a reflection of your financial trustworthiness and responsibility. Guarding that reputation should be a top priority, because the stakes have never been higher.

FAQs

How long does a missed payment stay on my credit report?

Missed payments can remain on your credit report for up to 7 years.

Will a single late payment really tank my credit score?

Yes, a single late payment can cause your credit score to drop by 100 points or more, depending on your overall credit history.

Can I get a late payment removed from my credit report?

In some cases, you may be able to get a lender to remove a late payment from your credit report if you act quickly and explain the circumstances.

- ➡The Fiery Bloom That Transforms Dull Borders into Stunning Masterpieces (You Have to See It to Believe It)

- ➡The Surprising Breathing Technique That’s Helping This 27-Year-Old Keep Her Cool in Stifling Meetings

- ➡The Shocking Truth About the Germ-Ridden Hotspot in Your Kitchen You Need to Know

- ➡The Secret Veggie Hack That Keeps Bread Fresh for a Week

- ➡Buried Treasure: The Shocking Discovery of Ancient Gold Hoards Hidden Kilometers Below the Earth’s Surface

- ➡Transforming an IKEA Spice Rack into a Stylish Entryway Furniture Piece

- ➡Forbidden Daylight Vanishes: The Shocking Race for the Best Eclipse View

- ➡Unlock the Secret to Lightning-Fast Fiber: Bouygues Telecom’s B&YOU Plan is a Game-Changer You Can’t Miss

How do I rebuild my credit after a setback?

Key steps include making all payments on time going forward, getting a secured credit card, and regularly monitoring your credit reports for errors.

Will a missed payment affect my ability to get a job?

Yes, many employers now check applicants’ credit histories as part of the hiring process, so a poor credit profile can hurt your job prospects.

How long will it take to recover my credit score?

The timeline for credit score recovery can vary, but generally it takes 6 months to a year of consistent on-time payments to start seeing significant improvements.

Can I still get approved for a loan or mortgage with bad credit?

Yes, but you’ll likely face higher interest rates and less favorable terms compared to borrowers with excellent credit.

- ➡Uranus Exposed! James-Webb Telescope Reveals Shocking Secrets of the Ice Giant

- ➡The Shocking Secret About How Often You Really Need to Change Your Sheets (It Will Blow Your Mind)

- ➡Shocking Trend: How Boring White Derbies Became Spring’s Hottest Shoes

- ➡Unblock Your Nose in Seconds: The Surprising Key Trick That Works Instantly

- ➡The Surprising Household Item Fueling Mould Growth (You’ll Never Guess What It Is!)

- ➡The Shocking Cardboard Hack That’s Transforming Gardens Across America This Spring

- ➡11 Perennial Plants That Desperately Need Fertilizer in March – Or Else Your Blooms Will Suffer

- ➡The Shocking Truth Behind the Rise of Banned Garden Pavilions and the Fines Imposed by Cities

Is there anything I can do to prevent a missed payment in the first place?

Setting up automatic payments, payment reminders, and communicating with lenders can all help you avoid accidentally missing a due date.